Ørsted says Maryland’s 966-MW Skipjack offshore wind project no longer makes financial sense

January 26, 2024

What Qualifications Do I Need to Become a Wind Turbine Technician?

February 1, 2024

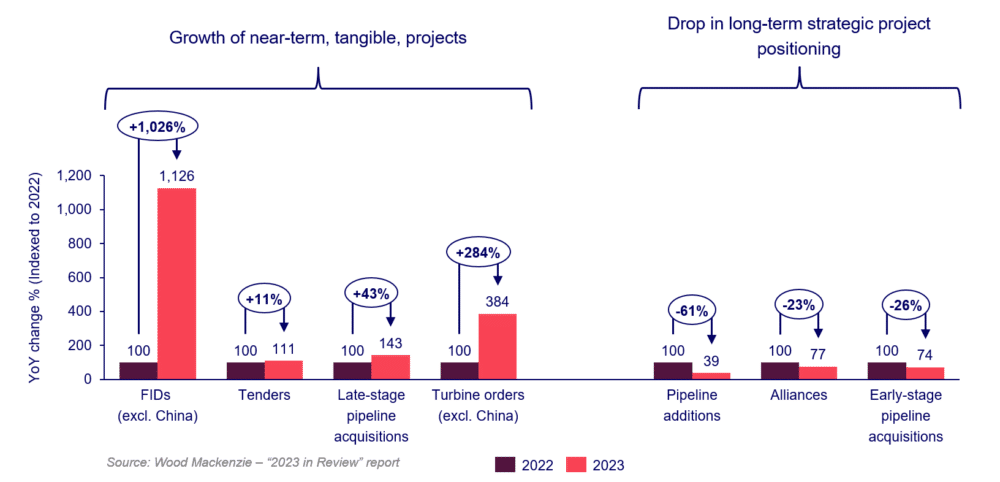

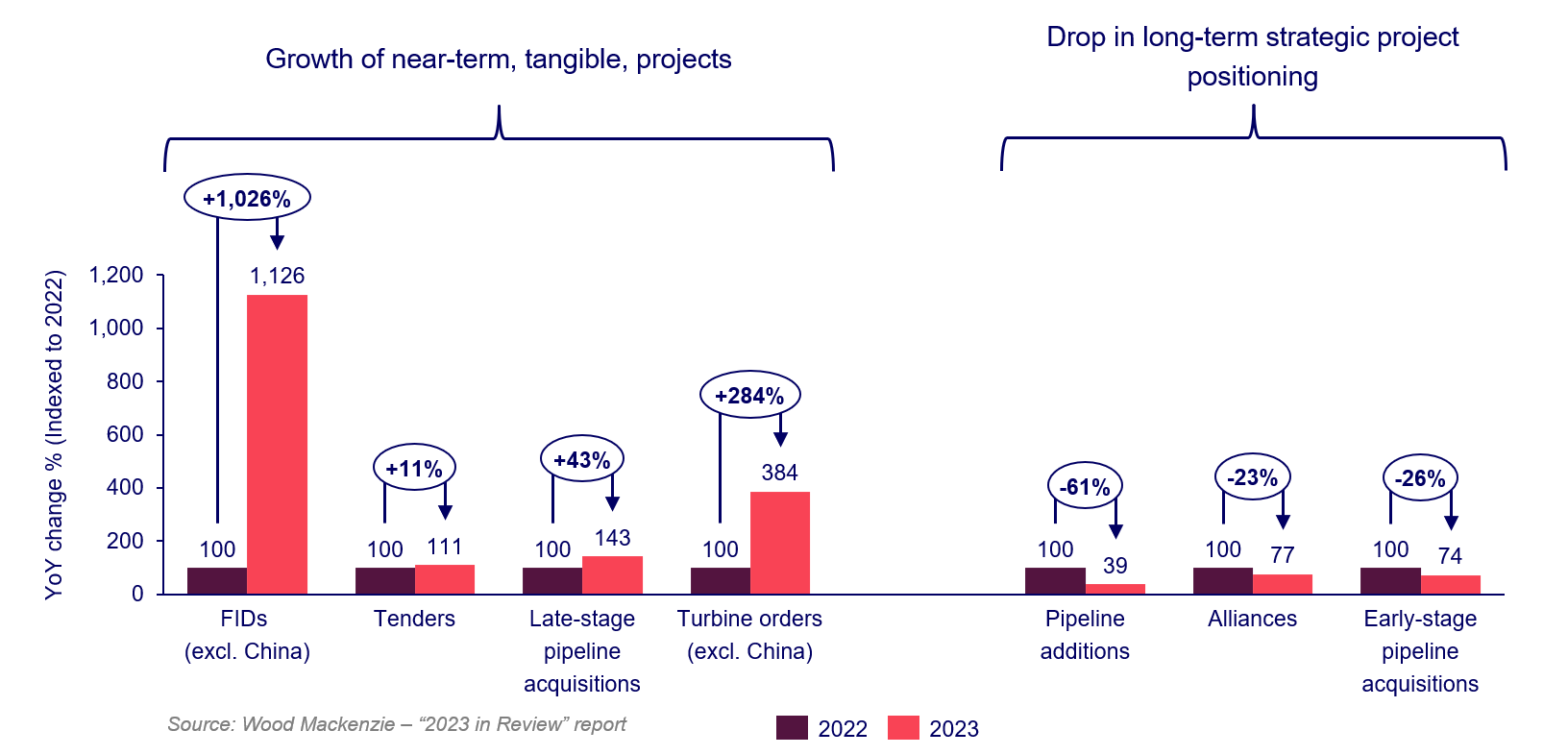

Despite supply chain headwinds and price pressures, the global offshore wind sector saw significant growth in its mature pipeline, as late-stage pipeline mergers & acquisitions (M&A), turbine orders and project financial investment decisions (FIDs) saw record activity in 2023. This has boosted the sector’s momentum into 2024, according to Wood Mackenzie’s ‘Offshore wind: 2023 in review’ report.

Headlines on headwinds countered by strong momentum into 2024

“Negative headlines for offshore wind were rife across much of 2023, as inflation and rising component pricing reversed the industries trend of continual cost reductions. With 8 GW of secured offtake cancelled, and zero participation in AR5 in the UK – which is the world’s largest offshore wind market excluding China – many would consider this a reality check for offshore wind,” said Finlay Clark, Senior Analyst at Wood Mackenzie.

“Yet going towards the end of the year, the sector gained momentum as developers doubled down on more tangible near-term opportunities – FIDs and turbine orders reached record levels, and both tender volumes and acquisition of advanced pipelines also increased compared to 2022. More importantly for 2024, governments across the globe offered the sector much needed tailwinds by announcing new and strengthened policy frameworks in Q4 2023,” Clark continued.

Credit: NYSERDA

Appetite for long-term opportunities faded

2023 experienced a year-on-year (YoY) drop of 61% in net annual pipeline growth, driven by a fall in project ambitions in emerging offshore wind markets. Fueled by falling technology costs in a rapidly globalizing market, capacity proposed in emerging markets ballooned in 2021 and 2022, stated the report.

Yet leading up to 2024, developers’ strategy became increasingly risk averse, placing a renewed focus on immediate tangible opportunities on core markets. This resulted in a drop in the number of alliances and early-stage project M&A activity, as fewer international developers and investors sought to establish links with new local players in higher risk markets.

“The necessary action taken by developers to target what is in front of them has increased the execution of established opportunities at the expense of those further afield,” said Clark. “However, despite a turbulent 2023, the sector finished the year with a healthy development pipeline of late-stage projects with an awarded support scheme, which was on par with the capacity at the start of the year, even with record FIDs and offtake cancellations.

Increased focus on near-term tangible opportunities

- Final investment decisions (FIDs)

The sector finished 2023 strong with a record 14 GW of FIDs. This was an 11-fold increase from 2022 to 2023, according to the report and nearly half of FID capacity in Europe was reached in Q4 alone as a flurry of activity in the UK and Polish markets drove activity to an all-time high by the end of the year.

“This is important as it increases the momentum for the industry going into 2024 and places an emphasis on delivering on these projects through secured contracts with suppliers and adhering to project timelines,” Clark added.

- Tender activity

A new record for awarded tender capacity was broken in 2023, with 31 GW awarded that year, a 13% increase YoY. Despite offtake challenges, competition also remained high as the number of bidders in tenders increased by 33%.

Europe witnessed significant tender activity totaling 13.6 GW, with Germany taking the lead through 8.8 GW awarded in 2023. Yet despite success in Germany, Europe’s total could have been higher if the UK had attracted bids in its AR5 auction, which yielded no participation due to caps on bid prices, which have subsequently been raised for allocation in 2024.

Clark added: “In addition to securing additional capacity, the German centralized tenders offer players an opportunity to win capacity for a direct route to market at the expense of high upfront capital cost. In 2023, we saw BP and TotalEnergies capitalize on this to cement their future in offshore wind through leveraging capital for these high-value tenders. These now offer the Majors’ a more streamlined development process which aligns with their ambitions for renewable energy growth. This success in German tenders has pushed them into the top five European offshore wind developers for awarded capacity.”

Despite a fall in total capacity exchanged, M&A activity for advanced pipeline projects grew to 10 GW, a 43% increase YoY. This brought new players to the offshore market, signaling continued competition and interest from institutional investors in the sector.

“The active M&A market assists developers with cashflow and allows them to recycle capital into future projects to continue to grow the offshore wind development pipeline,” stated Sasha Bond-Smith, Research Associate at Wood Mackenzie.

The average turbine ratings in China surpass Europe for the first time, stated the report. The global average turbine rating increased by 15% YoY, as the gaps between regional averages converge due to the continuous push for larger turbines in China.

“For turbine orders, 2023 was a record year for Europe and Asia Pacific (excluding China) and we also saw a big uptake in the U.S. With 11 markets landing turbine orders, including the first turbine order for Poland (of 1.1 GW),” added Bond-Smith.

- Grid-connected capacity

For grid-connected capacity, China added 6.7 GW in 2023 and now holds 49% of the global operational fleet, where the major Chinese asset owners were able to continue their ascent up the global rankings. Outside of China, annual grid-connected capacity fell to 4.2 GW, a 23% drop YoY from the record set in 2022, with Europe connecting just 2.9 GW, followed by the Asia Pacific (excluding China) with 1.3 GW.

“Installations in Europe could have been 88% higher outside of China. An additional 3.7 GW was initially targeted for grid-connection in 2023, yet project delays from transmission-related issues, combined with challenges in offshore construction and permitting, has pushed capacity into 2024,” said Clark.

- Policymaker ambition vs reality

Global targets for 2030 in offshore wind grew by 28 GW in 2023. However, sector headwinds combined with shifts in European energy demand forecasts and other power market fundamentals have widened the gap between Wood Mackenzie’s offshore wind outlook and 2030 government targets by 46% (YoY).

If the sector continues on this pathway, the offshore wind market will only reach 54% of 2030 global capacity targets (excluding China), according to Wood Mackenzie’s outlook.

Clark concluded: “2030 is only six years away – policymakers need to fast track processes and, in many markets, change their approach to reach their targets. This would include adjusting their targets. Higher targets do not mean more offshore wind capacity if not supported by a clear policy framework demonstrating a route to meeting these ambitions. It takes political courage to stomach this reality. However, it is a crucial step to allow the industry to believe that government ambitions are feasible and lowering targets will positively impact the offshore wind buildout in the 2020s.”

News item from WoodMac

Filed Under: News

{kind=link}

{kind=link}

{kind=link}